Even if you bought your home in the last few years, refinancing might make financial sense, if the numbers add up in your favor. Let’s look at the top factors to consider in home refinancing.

Do Your Homework…and Check it Twice

What’s your home’s value? Chances are, it’s changed since you purchased it. Online tools and in-person appraisers can help determine home value.

Ask your lender for an estimate of closing costs, as this number is key in determining the value of refinancing. What are current interest rates? The Consumer Financial Protection Bureau can help you there.

Refinancing usually hinges on the new payment amount. A refinance calculator can get you close to the eventual monthly dollar amount you’ll pay.

Consider All the Costs

A mortgage refinance will likely save you money in the long run. But to know exactly how much, you need to factor in the short-term costs. These may include appraisal, title and escrow fees, and credit fees.

Homeowners with less than 20% home equity usually have private mortgage insurance (PMI). Refinancing normally doesn’t affect PMI, but you will still want to check with your insurance provider.

Then there are taxes; often, the same tax deductions that apply to taking out a mortgage apply to refinancing. For example, mortgage interest is still tax deductible. But with refinancing, you may pay less in interest and thus have a lower tax deduction. Or vice versa. The closing costs of refinancing are generally not tax deductible. Tax implications for a cash-out refinance may differ from other refinancing options.

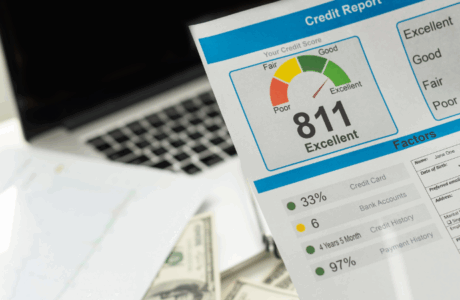

Know Your Credit Score

It may have changed since you first applied for your mortgage — and likely for the better! Then, as now, your credit score plays a significant role in getting approved for financing. A FICO score of 800 or higher is considered “exceptional,” 740 to 799 is “very good,” and 670 to 739 is “good.” It’s easy to get a free copy of your credit report.

Think Long-Term

And that means figuring out your refinance break-even point. You get that by dividing your initial costs by your monthly savings. It’s simple enough math but something many forget. The break-even point is especially important if you plan on moving soon, as you may not benefit from the savings if you move before the break-even date.

You don’t have to do all this alone. The loan experts at the Decker Group can help guide you through the refinancing process and answer all of your questions. Contact us online or call us at (972) 591-3097.

Comments are closed.