The short answer is simple: when it saves you money. How you save that money and how you might use refinancing for your financial benefit is a little more complicated.

When Interest Rates Are Lower

This won’t be the case for some homeowners, especially not those who bought homes during the coronavirus pandemic when rates hit historical lows in the 3% to 4% range. Today’s rates hover below 7%, and most experts believe mortgage rates will take only a slight dip into the mid-to-low 6% range through 2025.

If, however, you currently have a rate that’s above 7%, refinancing to get your mortgage into that mid-6% range might make sense. A mortgage refinance calculator can help you determine if refinancing will save you money.

When You Can Get Better Terms

Interest rate isn’t everything; many homeowners refinance to change their repayment terms.

For those who wish to pay their homes off sooner, they may refinance from a 30-year mortgage to a 15-year one. The monthly payments increase, but the homeowner saves in long-term interest and builds equity faster.

Some homeowners refinance in the opposite direction, going from a 15-year mortgage to a 25-year or a 30-year mortgage. Here, borrowers enjoy the benefit of lower monthly payments for paying more in interest over the life of the loan. But the latter isn’t necessarily the case; you can still pay off a 30-year loan early.

When You Want to Access Your Home’s Equity

This requires clear-eyed financial planning. Tapping into your home’s equity with a cash-out refinance can be an excellent way to reach a financial goal. You may wish to pay down high-interest debt, make an investment, pay for higher education, or achieve similar goals that require cash. With home improvements, you might use your home’s equity to increase your home’s value.

However, pulling cash out of your home means you increase the amount you owe on the loan and thus increase the interest you’ll pay long-term.

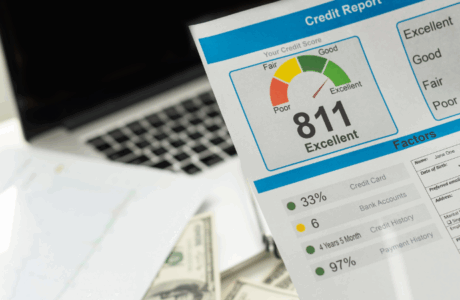

When Your Financial Profile Improves

For some homeowners, the terms of their original mortgages are based on financial profiles that no longer exist. But what if your credit score has considerably improved? Is your debt-to-income ratio much lower now? Then you might get better terms on a new mortgage loan. Even a 1% reduction in your mortgage rate could mean significant savings.

To talk about how refinancing might make financial sense for you, contact a member of the Decker Group at (972) 591-3097 or connect with us online.

Comments are closed.